Somewhere on your credit card statement is a box that most people never read, and it contains one of the most sobering pieces of math the federal government has ever required a company to print. It is the minimum payment warning, and it tells you, in plain numbers, how long you will be in debt and how much it will cost if you send only the minimum every month. For a typical carried balance, the answer is measured in years, sometimes decades.

That box exists because Congress decided consumers deserved to see the trap laid out in daylight. The minimum payment is not a suggestion about how to get out of debt. It is the smallest amount that keeps your account in good standing, calculated in a way that can keep a balance alive for a very long time. Understanding why is the first step to escaping it.

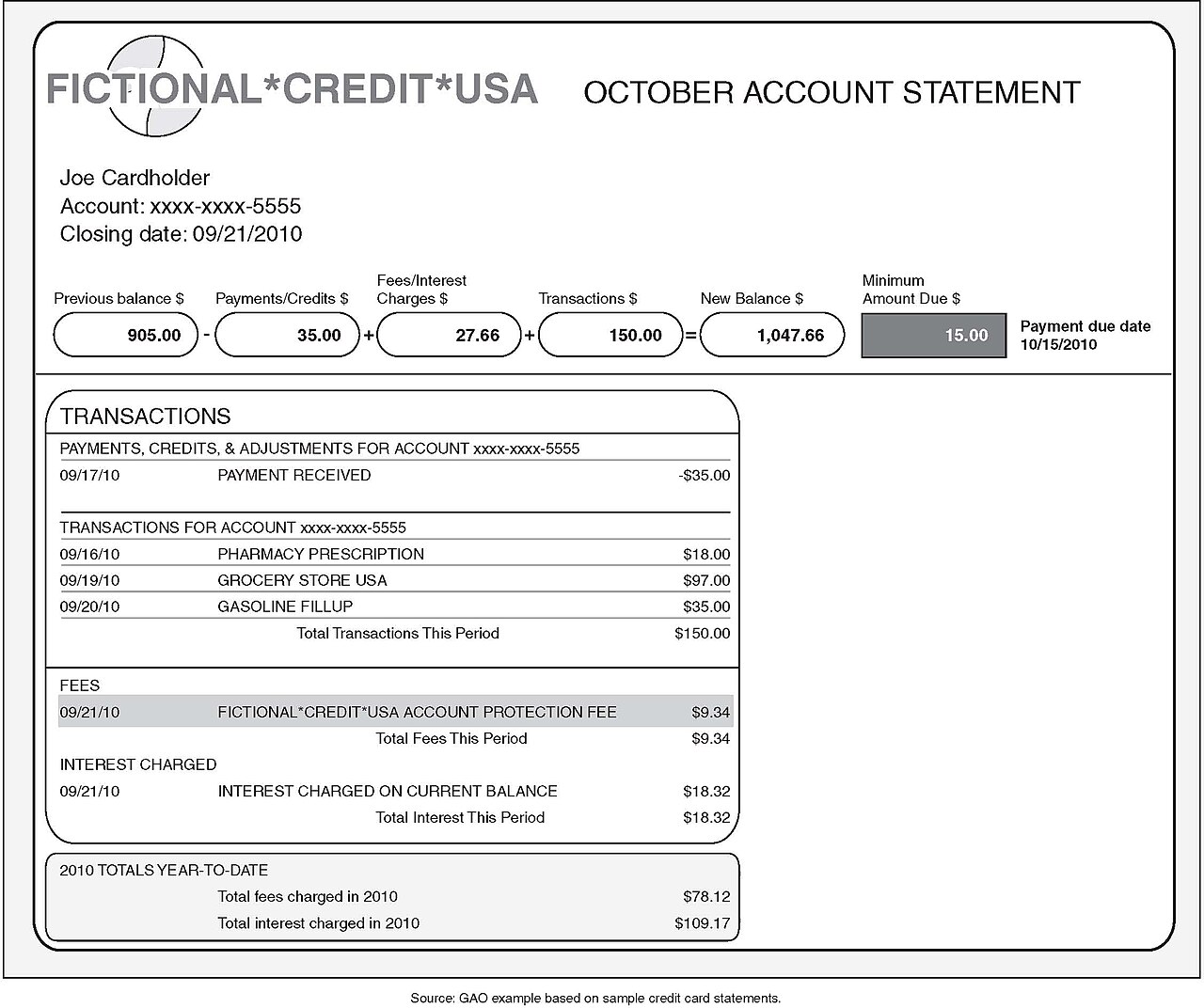

How the minimum is actually calculated

Card issuers set their own minimum payment formulas, but most follow a similar pattern: a small percentage of your balance, commonly in the low single digits, or a modest flat amount, whichever is greater, sometimes structured as a small slice of principal plus that month’s interest and fees. The Consumer Financial Protection Bureau’s credit card resources explain the mechanics and where to find your card’s formula in its agreement.

Notice what that design does. As your balance shrinks, the minimum shrinks with it, stretching the payoff further and keeping the interest meter running. The formula is built to keep the account current, and to keep the balance, the thing that earns the issuer interest, in place as long as possible.

Why so little of your payment touches the debt

Interest on a card compounds against you month after month. As an illustration, at a 22 percent annual rate, a $1,000 balance accrues interest at a rate of roughly $18 in a month. If your minimum payment that month is $25, about $18 of it goes to interest and roughly $7 actually reduces what you owe. You paid $25 and moved the debt by seven dollars. Next month, nearly the same thing happens again.

That is the whole trap in two sentences. Small payments mostly service the interest; the principal, the part that determines next month’s interest, barely moves. It is why people who faithfully pay the minimum for years can look up and find the balance barely changed, especially if new purchases keep landing on the card.

The warning box, and how to read yours

Since the CARD Act of 2009, issuers must print a minimum payment disclosure on every statement. The requirements live in Regulation Z, the federal Truth in Lending rules maintained by the CFPB. The box shows two scenarios: how long it takes to pay off your current balance making only minimum payments and what it costs in total, and, alongside it, the monthly amount that would clear the balance in three years and the total cost of doing that.

Read yours this month. The gap between the two totals is the price of the minimum payment habit, printed by the issuer itself. The three-year number is also a genuinely useful budgeting anchor: it is a fixed monthly figure, unlike the minimum, which drifts downward and drags the payoff out with it.

Breaking the pattern without heroics

You do not need to triple your payment overnight to change the math; you need to break the link between your payment and the issuer’s formula. A few workable approaches:

Pick a fixed amount and freeze it. If your minimum is $80 today, keep paying $80, or better, $100, every month even as the required minimum falls. Because the minimum shrinks and your payment does not, an ever-larger slice hits principal each month, and the payoff accelerates on its own.

Use the three-year number from your statement’s warning box as your target payment if it fits your budget. It was calculated for your exact balance and rate.

Aim any windfall, a tax refund, overtime, a side job’s proceeds, at principal. On a high-rate card, a lump-sum principal payment effectively earns you the card’s interest rate, which is a return no savings account will match.

And whatever amount you choose, autopay at least the minimum so a missed due date never adds a late fee or a penalty rate to the pile.

If the minimum itself is out of reach

When the budget will not cover even the required payment, do not simply skip it and hope. Call the issuer first: many have hardship programs that can lower the rate or payment temporarily, and asking does not require missing a payment first. A nonprofit credit counselor can also negotiate a debt management plan across all your cards. If an account has already gone to collections, the CFPB’s debt collection resources lay out your rights, and if an issuer treats you unfairly along the way, you can file a complaint with the CFPB.

The minimum payment is doing exactly what it was designed to do. The warning box on your statement is doing what it was designed to do, too: showing you the exit. The distance between “current” and “paid off” is the distance between those two numbers, and every dollar you pay above the minimum is a dollar that starts closing it.