Twenty-four percent. That is the flat slice a bank, brokerage, or client is required to carve out of certain payments and send straight to the IRS when something called backup withholding kicks in. It applies before you see a dime, it does not care what your actual tax bracket is, and for most people caught by it, the trigger was something as small as a typo on a form.

Backup withholding is the tax system’s insurance policy on income that normally arrives with no withholding at all: interest, dividends, freelance pay, broker proceeds. Usually you get the full amount and settle up at filing time. But if the IRS has reason to doubt it will ever see its share, it orders the payer to hold back 24 percent at the source. The IRS explains the program on its backup withholding page, and knowing the triggers is the whole game, because every one of them is fixable.

The most common trigger: a bad or missing taxpayer ID

When you open a bank or brokerage account or start work as a contractor, you hand over your taxpayer identification number, usually your Social Security number, on Form W-9. If you never provide the number, the payer must start backup withholding immediately. If you provide one that does not match IRS records (a transposed digit, a name that changed at marriage but was never updated with the Social Security Administration), the mismatch surfaces later and triggers the same result.

The mismatch route comes with warning shots. Under the IRS’s “B” notice program, the IRS notifies the payer of the mismatch, and the payer must send you a request to certify or correct your number. Ignore it, and the 24 percent begins. Fix it, and nothing happens at all. A surprising share of backup withholding cases are ultimately clerical: the form said one thing, the government’s file said another, and nobody reconciled them in time.

The second trigger: underreported interest and dividends

The other major pathway is behavioral. If the IRS determines you failed to report interest or dividend income on past returns, it can send notices ordering payers to begin backup withholding on those types of income going forward. This version is harder to shake, because it is not cured by a corrected form; it is cured by getting square with the IRS, filing or amending the returns in question, and receiving the agency’s confirmation that withholding can stop. The IRS also mails the taxpayer notices before this starts, so the 24 percent should never be the first you hear of the problem, provided your address is current.

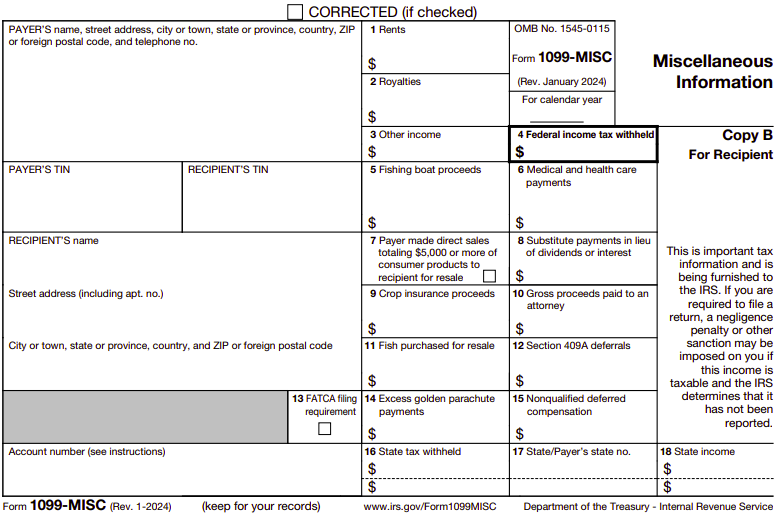

What income backup withholding can touch

The rules reach most payments that get reported on the 1099 series: interest (1099-INT), dividends (1099-DIV), nonemployee compensation for freelancers and gig workers (1099-NEC), rents and other payments (1099-MISC), broker and barter transactions (1099-B), and payment-app or marketplace proceeds reported on 1099-K, among others. Wages are not on the list; your paycheck already has its own withholding system. Notably exempt categories also include things like real estate sale proceeds and canceled debt, though the payer forms still get filed.

The money is not lost, but it is locked up

Here is the silver lining: backup withholding is withholding, not a penalty. Every dollar taken shows up on your 1099 forms (box 4, on most of them) as federal income tax withheld, and you claim it on your return like the withholding from any paycheck. If 24 percent was more than your real tax rate on that income, the difference comes back as part of your refund.

The catch is timing. The money leaves your hands the day you are paid and does not come back until you file for the year, which can be more than a year later. For a freelancer running thin margins, losing a quarter of every invoice to a fixable paperwork error is a genuine cash-flow problem, which is why the fix is worth doing the week you notice.

How to turn it off

Match the cure to the cause. If the trigger was a missing or mismatched TIN, submit a fresh, accurate W-9 to the payer, and if the underlying issue is a name change, update your records with the Social Security Administration so the databases agree. Payers can stop withholding once they have a certified, matching number. If the trigger was underreported income, respond to the IRS notice, file or amend what is missing, pay or arrange to pay, and the IRS will authorize payers to stop. In both cases keep copies, because you may need to show a payer the paper trail.

A two-minute audit that prevents the whole mess

Pull up your bank, brokerage, and payment-app profiles and check three fields: legal name, Social Security number, and address. Make sure the name matches what the Social Security Administration has on file, not a nickname or a pre-marriage name. If a client or platform ever asks you to complete or re-certify a W-9, treat it as urgent rather than junk mail. Backup withholding is one of the few IRS programs where the taxpayer holds every card: respond to the notices, keep the paperwork straight, and the 24 percent never leaves your account in the first place.